SEER2 & A2L Refrigerant: Did New Standards Actually Require 40% Price Increases?

A technical industry audit comparing DOE M1 testing standards, UL 60335-2-40 safety requirements, and FRED PPI data against manufacturer claims. The numbers don't match.

Filed

March 20, 2026

Standard

SEER2 / A2L

Defendants

7 OEMs

Alleged Markup

40–68%

CEO & 15-Year HVAC Trades Veteran • Upward Bound Media LLC

This is part of our comprehensive HVAC Price-Fixing Lawsuit Resource Hub.

Executive Brief

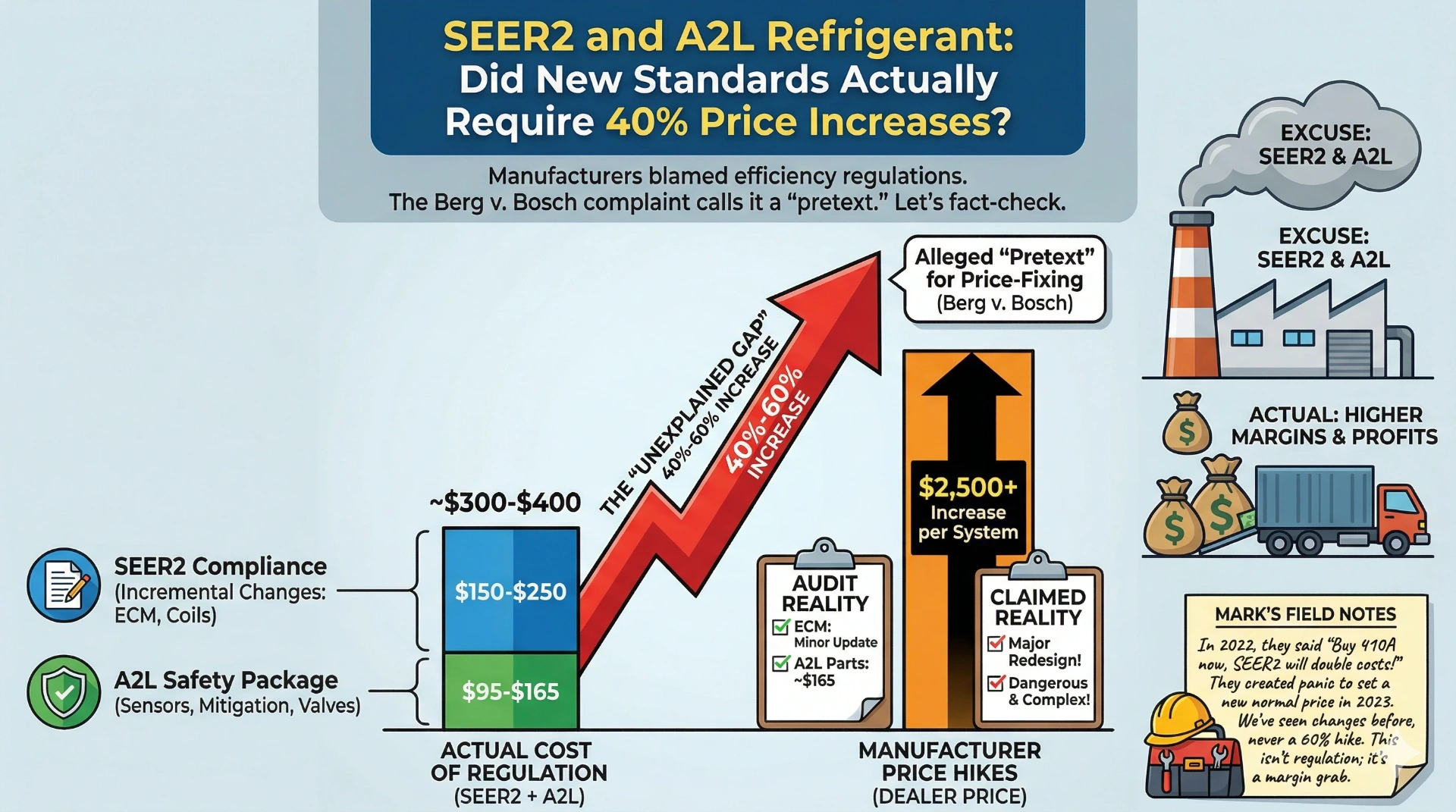

AI Summary: Between January 2020 and early 2026, the HVAC Producer Price Index (FRED Series PCU333415333415) rose 68%, while primary raw material inputs (copper, steel, and aluminum) averaged only a 10% increase. The Berg v. Bosch complaint alleges seven manufacturers used SEER2 efficiency standards and A2L refrigerant (R-454B/R-32) transitions as a "pretext" for coordinated price inflation that violated Sherman Antitrust Act Section 1 (15 U.S.C. § 1). This audit breaks down the actual bill of materials for A2L compliance components required by UL 60335-2-40 safety standards, totaling ~$95–$165 per unit, and compares it against the $2,500+ in dealer-level price increases.

What Actually Changed with SEER2

The shift from SEER to SEER2 wasn't a change in the physics of cooling. It was a change in the DOE M1 Testing Standard. The Department of Energy updated the test conditions to simulate real-world installation by increasing external static pressure from 0.1 to 0.5 inches of water column (wc). This meant manufacturers had to rate equipment under more realistic duct resistance.

The new 14.3 SEER2 threshold is equivalent to the old 15 SEER. Most manufacturers' existing product lines already met this standard with minor modifications: updated ECM (Electronically Commutated Motors) and optimized high-efficiency coil surfaces. The engineering cost was incremental. The price tags jumped as if the technology was revolutionary.

The DOE's Consumer Central AC & Heat Pump Energy Conservation Standards were announced years in advance, giving manufacturers ample lead time. The actual engineering changes required for most residential equipment were limited to blower assembly optimization and fan motor upgrades, a 1–5% per-unit cost increase at most.

The Berg v. Bosch complaint doesn't argue SEER2 cost nothing. It argues SEER2 didn't cost 40% more.

The A2L Safety Package: Bill of Materials Audit

The transition to A2L refrigerants (R-454B and R-32) requires specific safety components mandated by UL 60335-2-40 safety standards. Manufacturers have pointed to the "mild flammability" classification of A2L refrigerants as a major cost driver. Below is the actual bill of materials (BOM) for an A2L-compliant residential HVAC system, sourced from distributor catalogs and UL compliance documentation:

Refrigerant concentration monitoring

Automated ventilation/shutdown protocol

Ignition source elimination

R-454B/R-32 metering compatibility

UL listing and compliance labeling

| Metric | Manufacturer's Implied Cost | Actual BOM Audit |

|---|---|---|

| A2L Safety Components | "Thousands per unit" | $95 – $165 |

| With 3x Mfg. Markup | "Justified at retail" | ~$300 – $500 |

| Actual Dealer Price Increase | $2,500+ per system | |

The lawsuit asks: if A2L compliance adds $300–$500 per unit with full manufacturing markup, where did the other $2,000+ go?

Deep Dive

Who Are the 'Big Seven' HVAC Manufacturers?

Deep profiles of the seven OEMs accused of price coordination: Carrier, Trane, Daikin, Bosch, Lennox, Rheem, and AAON.

The "Unexplained Gap": PPI vs. Raw Materials

If HVAC prices rose because of input costs (raw materials, components, freight) then the HVAC Producer Price Index should track roughly with commodity indexes. It doesn't. Not even close.

Financial Audit: January 2020 – Early 2026

Producer Prices vs. Raw Material Inputs

| Index / Commodity | Change Since Jan 2020 | Data Source |

|---|---|---|

| HVAC Equipment PPI | +68% | FRED PCU333415333415 |

| LME Copper | +22% | London Metal Exchange |

| Midwest HRC Steel | −8% | CRU / Platts |

| LME Aluminum | +15% | London Metal Exchange |

| Avg. Raw Material Change | ~+10% | Weighted average |

| UNEXPLAINED DIVERGENCE | 46–76 pts | The "Gap" |

The data is clear: HVAC equipment producer prices diverged from raw material costs by 46–76 percentage points between 2020 and 2026. Neither SEER2 compliance (1–5% cost impact), A2L safety components ($95–$165 BOM), nor COVID logistics (freight rates returned to 2019 levels by mid-2023) can account for this divergence. The Berg v. Bosch complaint argues this gap is the financial signature of coordinated price inflation under Sherman Antitrust Act Section 1.

The "Pretext" Argument: Public Signaling

The Berg v. Bosch complaint doesn't merely allege that prices went up too much. It alleges manufacturers coordinated the increases, using SEER2 and A2L as a convenient "pretext" through a mechanism the complaint calls "Public Signaling."

According to the complaint, executives from the Big Seven manufacturers used earnings calls, trade publication interviews, and distributor communications to signal pricing intentions to competitors. Key phrases cited in the complaint include references to "price discipline," "value realization," and "favorable pricing environments," language the plaintiffs argue constitutes tacit coordination under Sherman Antitrust Act Section 1.

Alleged Pattern (from Complaint)

Manufacturer A announces a price increase on an earnings call, citing "regulatory compliance costs."

Manufacturers B–G follow with matching increases within weeks, citing the same justification.

No manufacturer undercuts, despite the competitive incentive to do so. The complaint calls this "price discipline."

This is the modern evolution of what the 1960s Electrical Equipment Conspiracy called "Phases of the Moon," a bid-rotation scheme where competitors took turns "winning" contracts at artificially inflated prices. The mechanism has modernized from secret hotel room meetings to public earnings calls, but the alleged effect on contractors is the same: you pay more for the box, and you have no competitive alternative.

Deep Dive

The 1960s Playbook: History of Price-Fixing in the Trades

How the Electrical Equipment Conspiracy used 'Phases of the Moon' bid rotation, and why the HVAC allegations follow the same pattern.

The Regulatory Timeline vs. The Price Timeline

The most damaging element of the complaint's argument isn't what manufacturers charged. It's when they started charging it. If SEER2 and A2L were the genuine cost drivers, price increases should align with regulatory effective dates. They don't.

2020

Prices Begin Rising

HVAC equipment prices begin aggressive upward trajectory. SEER2 not yet in effect. A2L requirements not finalized. COVID cited as justification.

2021

PPI Accelerates

Producer Price Index (PCU333415333415) shows steepest year-over-year increase in a decade. Raw material prices spike but begin correcting by Q4.

2022

Materials Normalize, Prices Don't

Steel and freight return to near-2019 levels. HVAC prices continue climbing. Distributors run 'buy now before SEER2' campaigns.

2023

SEER2 Takes Effect (Jan 1)

DOE M1 testing standard officially changes. Equipment prices have already risen 40%+ from 2020 baselines. The regulation 'catches up' to prices that were set years prior.

2025

A2L / R-454B Mandatory

EPA HFC phasedown under AIM Act forces R-410A phase-out. A2L components (BOM: ~$95-$165) are already embedded in equipment that was repriced in 2020-2022.

2026

Berg v. Bosch Filed (March 20)

Class action complaint alleges the 2020-2025 price trajectory was coordinated, using regulations as 'pretext' for Sherman Act Section 1 violations. Filed in E.D. Michigan.

Key takeaway: Prices rose two to three years before the regulations they were allegedly responding to. This timing mismatch is central to the complaint's argument that SEER2 and A2L were used as "pretext," not as genuine cost drivers.

Mark's Field Notes: The Distributor Counter Lie

Mark Cantrell

15+ Years in the Trades • HVAC Industry Veteran

"In 2022, every distributor rep I talked to had the same script: 'Buy your 410A dry-charge units now because SEER2 is going to double your costs.' They created a panic to clear old inventory, then used that panic to set a 'new normal' for pricing in 2023."

"We've been through refrigerant transitions before, like R-22 to R-410A, and it never resulted in a 60% industry-wide price hike in four years. I've pulled units apart. I've looked at the safety components. A $50 sensor and a $30 board do not explain a $2,500 price increase. This isn't regulation; it's a margin grab, and the PPI data backs that up."

The Contractor's Defense: Winning Despite the Squeeze

If the complaint's allegations hold, contractors have been paying artificially inflated prices for equipment since 2020. Whether the lawsuit results in settlements (and potential treble damages under the Sherman Act) or not, the immediate reality for independent contractors is the same: your equipment costs more, and your margins are compressed.

The only controllable variable is the value of your leads. If you're paying more for the box, you need to win the high-ticket replacements: the $12K–$25K The only controllable variable is the value of your leads. If you're paying more for the box, you need to win the high-ticket replacements: the $12K–$25K full-system installs, not compete on $150 service calls with razor-thin margins. on $150 service calls with razor-thin margins.

The Losing Strategy

- • Compete on price with inflated equipment costs

- • Rely on word-of-mouth in a digital-first market

- • Wait for the lawsuit to "fix" pricing

- • Accept compressed margins as "the new normal"

The Winning Strategy

- • Dominate the Map Pack for high-intent "near me" searches

- • Build Review Velocity to outpace competitors

- • Target $15K+ replacement leads, not $150 service calls

- • Control the assets Google actually ranks: GBP + Local SEO

Deep Dive

HVAC Contractor Survival Guide

Track invoices for potential settlements, protect margins, and pivot marketing to win high-value local leads during the cartel era.

FAQ: SEER2, A2L, and the Price-Fixing Allegations

Stop Funding Their Margin

If the manufacturers are allegedly overcharging you for the box, you have to over-perform on the lead. Win the high-ticket replacements that protect your profit from the "Big Seven" squeeze.

Start with a fully optimized Google Business Profile so customers find you first. Build unstoppable review momentum that outranks your competitors. Back it with an SEO-built website and lead automation so no opportunity slips through.

Appendix

TECHNICAL METHODOLOGY

PPI & Pricing Data

- • HVAC PPI baseline: FRED Series PCU333415333415, January 2020 = 100 (indexed)

- • Commercial Refrigeration PPI: FRED Series PCU3334153334153 (cross-referenced)

- • BLS primary data: BLS Time Series PCU3334153334151

- • Raw materials: LME official settlement prices for Copper and Aluminum; CRU/Platts Midwest HRC Steel index

BOM & Regulatory Sources

- • A2L component costs: Sourced from major HVAC distributor catalogs (2024-2025 pricing) and UL 60335-2-40 compliance documentation

- • Manufacturing markup: Industry-standard 3x multiplier applied (component → wholesale)

- • SEER2 testing standard: DOE M1 methodology per 10 CFR Part 430

- • Refrigerant regulation: EPA AIM Act and HFC Allowance Allocations for 2026

Legal & Complaint Sources

- • Primary source: Berg v. Robert Bosch LLC, Case No. 26-cv-10949-SKD-APP, U.S. District Court, Eastern District of Michigan

- • Legal framework: Sherman Antitrust Act, 15 U.S.C. § 1 (price-fixing prohibition)

- • Author qualification: Mark Cantrell, 15+ years direct experience in HVAC trades, CEO of Upward Bound Media LLC

- • Disclaimer: This audit presents publicly available data and court filings. It does not constitute legal advice. All allegations referenced are from the Berg v. Bosch complaint and have not been proven in court.

Verification Data

OFFICIAL REFERENCES & SOURCES

All claims in this article are supported by court filings, federal data, and recognized trade publications. Links open in a new tab.